What is a Capital Gain?

To understand capital gains tax, it is first important to understand capital gains. A capital gain is the increase in value of something you own, also called an asset. For example, let’s say you purchase a collector vehicle for $2,000. Two years later, after enjoying the vehicle and keeping it in good condition, you are pleased to learn the value has increased to $3,000. If you decide to sell the vehicle, the difference between your basis (what you paid) and the sale price would be a capital gain. In this instance the capital gain would be $1,000. It applies to tangible and intangible assets, such as rental properties, stock, currency, etc. Most of the items we purchase typically decline in value, such as non-collector vehicles, so we only have to worry about capital gains tax on items that appreciate in value.

How is a Capital Gain Taxed?

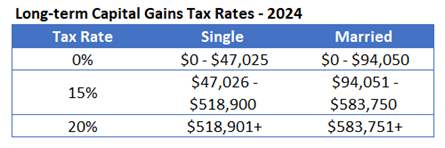

A capital gain is taxed differently than your income. Income is taxed at what is called your ordinary income rate. These are the taxes that are either deduced from your paychecks if you are an employee or paid quarterly directly to the IRS if you are self-employed. A capital gain is taxed at different rates depending on how long you held the asset before selling it. A long term capital gain is an asset that was held for more than one year. A short-term capital gain is held for less than one year. A short-term gain is taxed at the individuals ordinary income tax rate during the year in which it was sold. Long-term capital gains rates are more favorable than income tax rates, but similar to income tax rates, will increase as you earn more money in any given year. Below are the long-term capital gains tax rates for 2024. Again, note that short-term capital gains rates are taxed as ordinary income.

Primary Residence Exclusion

Home ownership is a vital part of the American economy. It is important that home owners are not penalized when selling their homes if the value of their home has increased since purchase. If you have a capital gain on the sale of your home, the first $250,000 of that capital gain is not taxed. If filing taxes jointly with a spouse, this exclusion doubles to $500,000. In order to qualify for this exclusion, you must have occupied the home for an aggregate of two out of the previous five years. If you have not, the entire gain is subject to capital gains tax. This rule is in place to ensure that home-flippers are not taking advantage of this exclusion.

To illustrate how this exclusion works here are a couple of examples.

Jim and Pam purchased a home in Austin, Texas in 2014 for $300,000. Two years later, they decide to move closer to their daughter CeCe’s school. They sell their home for $600,000. They do not owe any capital gains tax since they file their taxes jointly.

Shortly after getting married in 2012, Michael and Holly purchased a home in Boulder, Colorado for $200,000. Over the next six years they have four children and need a larger home. They are surprised to learn that the value of their three bedroom ranch has increased to $800,000. They file their taxes jointly, so they are able to claim the primary residence exclusion for the first $500,000 of the gain. However, since the increase in value was larger than the exclusion by $100,000, they must pay capital gains tax on that amount.

Why are Capital Gains Important?

It is important to understand Capital Gains, especially when filing your taxes. Individuals holding appreciating investment properties, stock, jewelry, or other capital assets must understand the implications of selling these assets.

How do I Minimize Capital Gains Taxes?

Invest in a retirement account. Your 401(k), 403(b), IRA, or other retirement account is a huge asset in avoiding capital gains tax. All gains inside of a qualified retirement account grow tax free, meaning there are no capital gains assessed on the growth of the investments within the account and distributions are tax-free.

Tax Loss Harvesting: If you lost money on the sale of a capital asset, you can use that loss to offset gains. For example, Danny purchased Stock A for $300 in 2022. It is now worth $600. On the same timeline, he also purchased stock B for $600, but it decreased to $300. If he chooses to sell both within the same year, he can offset the entire gain with the loss and not pay any taxes. This can be a useful tool from year to year if someone owns many capital assets. If the loss from the sale is greater than the capital gain, up to $3,000 can be counted against ordinary income. For example, If Danny’s stock B decreased to $100, he could avoid paying Capital Gains on his sale of Stock A and also offset $200 against his salary. That’s $200 he won’t have to pay taxes on.

In summary, I do want to point out that although it can be painful to pay capital gains tax, it always means you made money on an asset, which is inherently a good thing.

As always, if you have any questions or need any assistance navigating finances, please reach out to us at Perry Financial Group.

Until next time,

Joe Perry